The Great Consolidation: Why On-Demand Healthcare Staffing Must Restructure to Survive

- Greg Paulus

- Jan 14

- 8 min read

A sober look at M&A, margins, and what comes next for on-demand nursing

After spending the last few years working deeply in the on-demand nursing space with several of the larger platforms, IntelyCare’s acquisition of CareRev is exactly the kind of move I’ve been expecting as this market matures. But it’s not just the beginning of a classic growth-driven roll-up story. It’s the early signal of something more fundamental: a sector that has come off its pandemic highs, is wrestling with a structurally different margin profile, and now needs consolidation as much for survival as for scale.[1][2][3]

For C‑suite healthcare executives and private equity professionals, this isn’t about chasing the next exuberant valuation. It’s about understanding which platforms have the economics, technology, and customer relationships to justify additional capital and which ones will need to merge, pivot, or wind down over the next 24 months.[4][5]

The Market Is Big and Growing – But the Cycle Has Turned

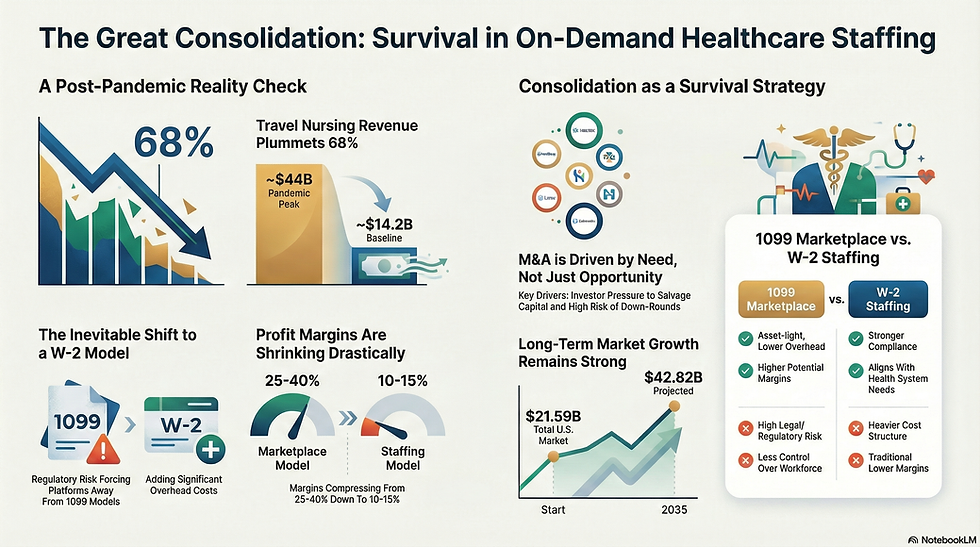

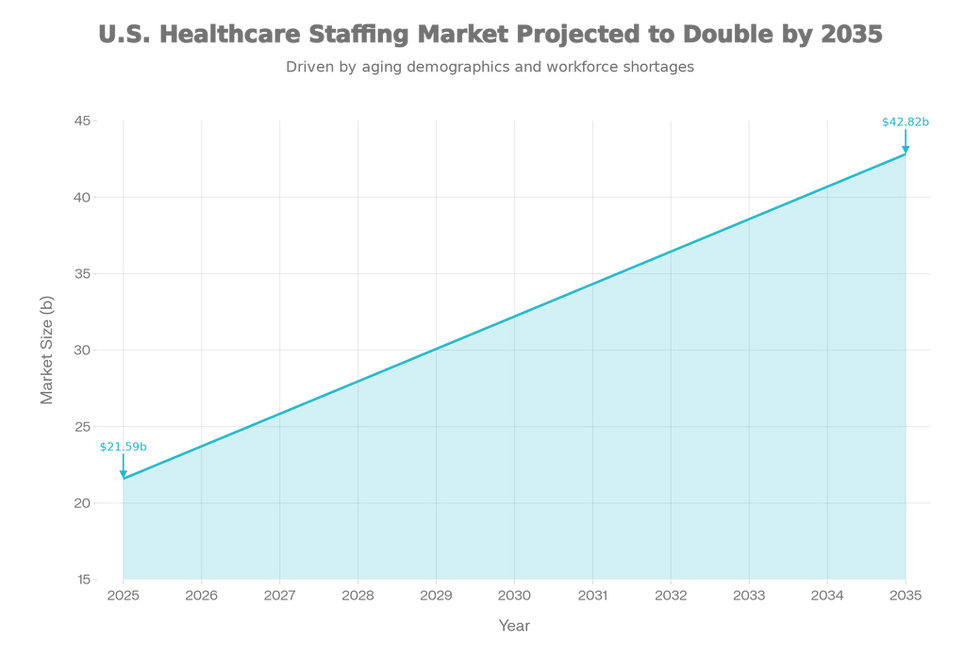

The top‑line story remains compelling. The U.S. healthcare staffing market is valued at approximately USD 21.59 billion in 2025 and is projected to reach USD 42.82 billion by 2035, with a 7.09% CAGR, driven by demographics, persistent workforce shortages, and ongoing care-delivery transformation.[3]

Beneath that growth curve, however, the cycle has sharply shifted from the pandemic era:

Travel nursing revenues surged to an estimated 44 billion USD peak during the pandemic and have since normalized back to around 14.2 billion USD, a 68% contraction.[2][6]

Shortages remain structural: an estimated 263,870 unfilled RN positions nationally (8.06% shortage), and LPN shortages projected to worsen from 20% in 2026 to 28% by 2036.[7]

Healthcare organizations are reacting by building internal capacity first—float pools, internal resource pools, and system‑wide PRN programs—before turning to third‑party agencies and on‑demand platforms.[6][8]

At the same time, technology adoption is accelerating: more than 80% of staffing revenue now flows through MSP/VMS channels, and 90%+ of executives expect to adopt platforms within five years.[9][2]

In other words: demand is still there, but the “easy money” phase is over. Health systems are more cost‑conscious, internal‑first strategies are maturing, and external platforms must deliver value under normalized rates and tighter margin constraints.[5][10]

Where the Dollars Are – and Aren’t – Now

The staffing ecosystem is not monolithic. Different segments face different economics and consolidation pressures:[2][9]

Market segment breakdown showing travel nursing ($14.2B), locum tenens ($9.6B), per diem ($4.5B), and VMS/MSP technology ($3.5B) as key consolidation targets.

Travel Nursing – 14.2B USD (down from ~44B) - Post‑pandemic normalization has hit this segment hardest. Margins once buoyed by crisis‑level bill rates are now compressed, even as operating costs remain high.[2][6]

Per Diem – 4.5B USD - Core territory for on‑demand nursing platforms. Attractive for flexible scheduling and local fill‑ins, but increasingly subject to internal competition from hospital float pools and PRN programs.[8][2]

Locum Tenens – 9.6B USD, ~5% annual growth - Physician and advanced practice shortages keep this segment resilient. It remains fragmented and is a natural target for specialty roll‑ups.[9][2]

VMS/MSP Technology – High‑growth infrastructure - VMS/MSP platforms supporting contingent workforce are growing around 13–14% CAGR, with 80%+ of revenue already flowing through these channels. The “pipes” of staffing—rather than the agencies alone—are where significant enterprise value is accruing.[2][9]

The opportunity is real, but it is unevenly distributed. Platforms that fit cleanly into system‑wide workforce strategies, integrate into VMS/MSP ecosystems, and help health systems reduce total labor spend will be positioned to participate in this growth. Others will not.[6][11]

The Economic Reality: Consolidation as a Survival Strategy

During the pandemic, many on‑demand platforms enjoyed a rare combination: surging demand, extraordinary bill rates, and a lean marketplace cost structure. Those conditions have reversed.[2][12]

Two structural shifts are now front and center:

1. The W‑2 Model Is Becoming Non‑Optional

The legal climate around worker classification is tightening. Several platforms have moved—or are moving—toward W‑2 employment models as a defensive strategy against misclassification risk.[13][14]

W‑2 has clear advantages:

Stronger legal footing and regulatory compliance

Better alignment with health systems’ expectations around oversight and quality

Greater control over workforce, scheduling, and reliability

But it comes at a cost:

Payroll taxes, benefits, workers’ compensation, and HR overhead

Margin compression from marketplace‑style 25–40% take rates down to more traditional 10–15% staffing margins

For many on‑demand companies, especially those designed as asset‑light marketplaces, this shift has fundamentally altered unit economics.[6][14][13]

2. Rates Have Normalized, But Cost Structures Haven’t

As federal COVID relief has wound down and health system budgets have tightened, bill rates and pay packages have come back to earth. At the same time:[6][9]

Talent still expects above‑pre‑pandemic flexibility and compensation

Platforms carry heavier W‑2 cost structures

Customer acquisition costs remain high in a crowded, fragmented market

The result is what many insiders are now asking: “Is the current economic model sustainable without significant growth in customer base and deep cost synergies?”

Valuations: Last-Round Marks vs. Today’s Reality

Much of the ecosystem’s valuation narrative still references the last capital raise—almost all of which occurred between 2021 and 2023, in the midst of crisis‑level demand:

ShiftKey – ~2B USD valuation after a major raise backed by Lorient Capital (2023)[15][16]

IntelyCare – ~1.1B USD valuation with a 115M USD Series C (2022)[17][18]

Incredible Health – 1.65B USD valuation on an 80M USD Series B (2022)[19][20]

Clipboard Health – 1.3B USD valuation with 80M USD in total funding (2022)[21][22]

These marks reflected pandemic‑era economics and a very different risk appetite for growth‑stage digital health and labor platforms. With travel nursing volumes down ~68% and tech valuations broadly corrected, it is reasonable to assume current fair values are materially lower.[2][5][12][23]

For clarity, any valuation references should be explicitly framed as:

“Last known post‑money valuations at time of most recent funding round (2021–2023), not current mark‑to‑market values.”

This distinction matters for investors eyeing M&A. The consolidation wave ahead is less about defending unicorn valuations and more about rationalizing capacity, salvaging capital, and creating one or two durable platforms per segment.[4][24]

Business Model Reality: 1099 vs W‑2

To understand who survives and who consolidates, we need to distinguish the dominant models:

1099 Marketplace Models

Pros:

Asset‑light, lower overhead

Potentially higher contribution margins in high‑rate environments

Highly attractive during surge demand

Cons:

Legal and regulatory risk (worker classification, benefits)

Increasing scrutiny from regulators and health systems

Less control over workforce engagement and consistency

W‑2 Staffing Models

Pros:

Stronger compliance posture

Better alignment with health system governance and risk appetite

More control over assignment quality, scheduling, and retention

Cons:

Heavier cost structure (benefits, payroll tax, workers’ comp)

Traditional staffing‑like margins (10–15%), not marketplace margins

Requires significant scale to achieve acceptable EBITDA

Consolidation implication: Surviving platforms will likely be hybrid in practice—using 1099 where legally and strategically appropriate (e.g., short‑term per diem, certain states) and W‑2 where regulatory and customer risk is highest (e.g., longer assignments, sensitive markets). Those unable to reach scale under W‑2 economics, or to defensibly maintain 1099 models, will be prime candidates for consolidation.[2][13]

Consolidation Drivers: Liquidity, Not Just “Upside”

It is tempting to frame the coming M&A wave purely as a growth story: bigger platforms acquiring smaller ones to seize market share. The reality is more nuanced.[5][23]

Several forces are pushing consolidation from the investor side:

Aging vintages: Many platforms raised their largest rounds in 2021–2022. PE and growth equity funds are now in the 3–5-year window, when they must decide whether to double down, force a sale, or prepare for down rounds.[4][5]

Down‑round risk: Raising new capital at lower valuations is often unpalatable and highly dilutive to founders and early investors. Strategic M&A—even at a lower multiple—can be more attractive.[23][24]

“Capital salvage” mindset: For some investors, the realistic goal is not a 3x outcome but to recover a meaningful portion of their invested capital through mergers, recapitalizations, or sales to strategic buyers.[28][4]

From the operating company side, the drivers are equally pragmatic:

Subscale W‑2 platforms are facing structurally thin margins with limited ability to cut costs further

1099 marketplaces are facing growing classification risk and customer preference for more integrated, accountable partners

Health systems consolidating their vendor rosters and pushing volume to fewer, more capable partners[6][5]

In short: consolidation is coming not just to capture upside—but to avoid an extended, value‑destroying grind.[5][28]

A More Grounded M&A Thesis: Where Deals Still Make Sense

Against this backdrop, M&A can still create substantial value—but only when it squarely addresses the new economic reality.

For private equity and strategic buyers, three themes are critical:

Scale to Restore Margins

Consolidating back‑office operations, credentialing, and compliance across multiple platforms

Rationalizing overlapping tech stacks into one integrated platform

Negotiating better rates and terms with health systems and payers

Integration Into Health System Strategy

Sharper Target Selection

Strategic assets: differentiated tech, strong NPS, deep enterprise relationships, proven ability to support internal‑first strategies

Distressed assets: commodity marketplaces, weak enterprise penetration, limited differentiation, heavy burn

Deals that don’t explicitly address these will struggle to deliver acceptable returns in the current environment.

How WonWay Health Fits Into This Picture

Over the last three years, we’ve had the privilege of working directly with several of the most recognized names in this sector—ShiftMed, ShiftKey, and connectRN—and previously advising Incredible Health through a period of rapid growth. That experience, combined with 60+ years in broader healthcare and health tech, has shaped a grounded view of what will and won’t work in this next phase.[13][14][30][31][32]

Where we help PE and strategic acquirers:

Pre‑deal diligence: Assessing not just TAM and growth stories, but real unit economics, customer stickiness, and operational maturity.

Model viability assessment: Evaluating whether a target’s W‑2/1099 mix, pricing power, and sales efficiency can sustain itself post‑pandemic, or needs structural change.

Integration and value‑creation plans: Designing GTM integration, sales structure, account ownership, and cross‑sell strategies that actually get executed in the field—not just in PowerPoint.[31][32]

Anchor customer strategy: Leveraging health system relationships and experience to secure or protect anchor clients that de‑risk the investment.[32]

In a market where the headline growth story is now widely understood, the differentiation lies in operational insight and realism.

Why 2026–2027 Matters

The next 18–24 months are pivotal for on‑demand nursing and broader healthcare staffing platforms:

Pandemic‑era funding vintages are reaching critical decision points.[4][5]

Health systems are formalizing internal‑first workforce strategies and vendor rationalization plans.[6][8]

W‑2 economics are forcing platforms to either scale rapidly, consolidate, or rethink their models.

Regulatory and legal pressures around classification and fairness in labor markets are increasing.[24][33]

For some platforms, this will be the time to lead consolidation—to become the acquirer, not the acquired. For others, this will be the moment to seek the right partner and integrate into a stronger platform rather than run down a runway in isolation.

For investors, it is the moment to separate signal from noise: to distinguish structurally sound, strategically placed assets from those whose models were fundamentally tied to a once‑in‑a‑century demand spike.

Closing Thoughts

The on‑demand nursing story is no longer just about growth and disruption; it is about restructuring, integration, and sustainability. The consolidation ahead will be messy in places, and not every outcome will be a headline‑worthy win. But for those who approach it with clear eyes—grounded in real economics, regulatory reality, and health system behavior—there is still substantial value to be created.

If you’re a PE investor, strategic buyer, or operator navigating this next phase, we’d welcome a conversation about what you’re seeing and where you’re wrestling with uncertainty. This is exactly the juncture where thoughtful, operator‑led insight can prevent expensive mistakes—and help the right platforms emerge stronger on the other side.

This article reflects views and interpretations of publicly available information as of January 2026, and is intended for informational purposes only. It should not be taken as investment advice or as a statement of current valuation for any specific company.

https://www.precedenceresearch.com/us-healthcare-staffing-market

https://www.definitivehc.com/blog/healthcare-staffing-trends

https://www.hallmarkhcs.com/healthcare-staffing-report-2025/

https://www.healthcaredive.com/news/top-healthcare-provider-trends-2026/809077/

https://www.healthcarousel.com/post/workforce-planning-flexible-healthcare-staffing-and-models

https://www.shiftkey.com/resources/news/shiftkey-lorient-capital-funding

https://www.incrediblehealth.com/blog/series-b-funding-2022/

https://kpmg.com/us/en/articles/mergers-acquisitions-trends-healthcare-life-sciences.html

https://www.law.georgetown.edu/denny-center/blog/medicine-private-equity/

https://nursa.com/blog/nursa-leverages-80m-to-address-nursing-shortage

https://www.trustedhealth.com/press-articles/trusted-series-c

Comments